Inheritance Tax Planning

Inheritance tax and estate planning sit right at the meeting point of money, love and legacy. For many people this feels like unfamiliar territory. It can stir up anxiety, confusion or even family tension.

Thoughtful planning with a financial adviser can turn all of that into something very different. It can become a calm, kind and intentional process where you decide what you want your money to do for the people and causes you care about.

What most people want help with

“Will my family face a big tax bill when I die”

Common worries:

Not knowing how inheritance tax works or whether it will apply.

Hearing scare stories in the media and assuming the worst.

Owning a family home that has grown in value and wondering if that alone might trigger tax.

A financial adviser will:

Explain clearly when inheritance tax is and is not due.

Estimate the potential tax bill on your current estate and model different scenarios.

Show how existing allowances and exemptions can reduce or even remove the tax due, for example through the standard inheritance tax threshold (£325,000 per person) and the residence allowance (£175,000 per person) are currently frozen until at least April 2028.

Work alongside your solicitor so that your will, trusts and any life assurance policies all pull in the same direction.

The result is that uncertainty is replaced by a clear picture and a plan.

“I want things to be fair between my children but our situation is complicated”

Common worries:

Blended families where there are children from previous relationships.

One child is more vulnerable or less financially secure than the others.

Some family members help more with care and the parent wants to recognise that.

A financial advisor can:

Help you explore what “fair” really means for you, rather than assuming it must mean “equal”.

Use cash flow planning to show how much you are likely to need in your own lifetime so you know what is safely available to pass on.

Work with you and your solicitor to design wills and trusts that reflect your wishes while aiming to minimise conflict later.

You gain a structure that balances head and heart and gives your family clarity.

“I am worried about protecting a vulnerable person”

This might be a child or adult with additional needs, a family member who struggles with money, or someone who is at risk in relationships.

A financial advisor can:

Explain how certain types of trust can hold money for a vulnerable person, with trustees responsible for managing and releasing funds for their benefit.

Coordinate with a specialist solicitor to build these arrangements into your will or wider plan.

Ensure that investments and insurance policies are structured to support this trust based approach.

This protects the person you care about without simply handing them a large sum to manage on their own.

“I do not want my partner to be left exposed”

Common worries:

You are not married or in a civil partnership and assume your partner will automatically inherit.

Your main asset is your home and you are concerned your partner could be forced to sell.

In England and Wales, unmarried partners do not inherit automatically under the intestacy rules

A financial advisor will:

Point out where a partner has no automatic rights and highlight the urgency of making a will.

Help you decide how best to provide for a partner, whether through your will, life assurance, pensions or trusts.

Encourage you both to put Powers of Attorney in place, so either of you can manage money or make health decisions if the other loses capacity.

This kind of planning can be the difference between security and real hardship for a surviving partner.

“What if I lose mental capacity and my family cannot access my money”

Common worries:

Dementia and other illnesses that affect decision making.

The fear of being a burden.

Adult children not knowing how they would pay for your care or keep the household going if you could no longer manage your own finances.

Advisers make Powers of Attorney a routine part of planning and can:

Explain the different types and how they work.

Help you think through who to appoint and how to balance family dynamics.

Coordinate with a solicitor to get the documents drafted and registered while you are still well

That way your values and preferences guide decisions even if you are not able to speak for yourself at some future point.

A simple overview of inheritance tax in the UK

Inheritance tax is a tax on the value of a persons estate when they die. The estate usually includes:

Property

Savings and investments

Personal belongings

Some life assurance policies if they are not held in trust

It can also apply to certain gifts made during your lifetime, especially those made in the seven years before you die. The rules change over time but the key ideas are:

Each person has a standard inheritance tax threshold, often called the nil rate band. The current level is three hundred and twenty five thousand pounds and tax is only charged on the value above this threshold.

Many estates also benefit from an additional allowance called the residence threshold when a home is left to direct descendants such as children or grandchildren. This allowance is currently one hundred and seventy five thousand pounds per person and is also frozen until at least April twenty twenty eight.

Unused portions of your allowance can usually be transferred to a surviving spouse or civil partner, meaning couples can often pass on up to double the combined thresholds before inheritance tax is due.

Amounts above the available thresholds are generally taxed at forty per cent on death, though this can reduce to thirty six per cent where a sufficient share of the estate is left to charity. A financial adviser can:

Explain how these allowances apply in your situation.

Help you make use of lifetime gifting allowances.

Work with your solicitor and accountant to design a plan that aligns with current legislation and can be updated as rules change.

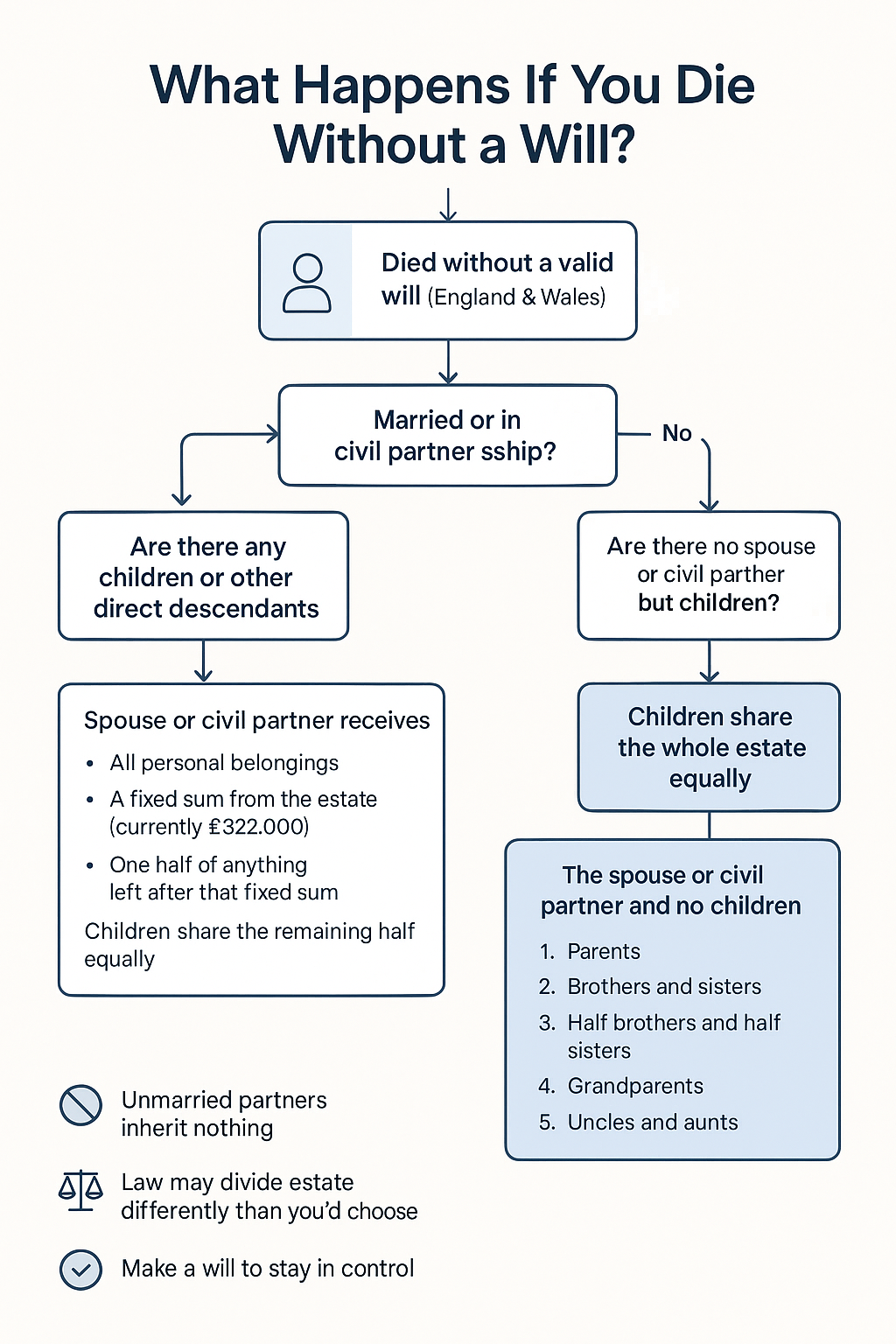

What happens if you die without a will

Dying without a valid will is called dying intestate. In that case, your estate is shared out using a strict legal order. Your personal wishes, promises and understandings within the family are not taken into account. The rules vary across the United Kingdom. The outline below is for England and Wales.

Partnership has 2 s’ here!!

Trusts in estate planning

What is a trust

A trust is a legal arrangement where one person transfers assets to trustees to look after for the benefit of other people. In UK law:

The person who provides the assets is called the settlor.

The people who manage them are the trustees.

The people who may benefit are the beneficiaries.

The assets in the trust might be cash, investments, property or even a life assurance policy. Different types of trust are taxed in different ways and can be quite technical, which is why professional advice is essential

Why you might use a trust

Some common reasons:

To provide for young children without giving them large sums outright at eighteen.

To protect family wealth where beneficiaries are vulnerable, at risk of divorce or have challenges around addiction or debt.

To hold life assurance proceeds outside your taxable estate.

To support several generations over time, allowing trustees to decide when and how to help.

How a financial adviser adds value with trusts

A financial advisor can:

Explore with you whether a trust structure genuinely serves your aims and whether the additional complexity is justified.

Work closely with a solicitor so that the trust deed, your will and your investments are all aligned.

Make sure any trust that needs to be registered is registered correctly and that trustees understand their ongoing responsibilities.

This combination of financial planning and legal structure can bring a great deal of comfort that your money will be managed in the spirit in which you leave it.

Powers of attorney

What are powers of attorney

A Power of Attorney is a legal document by which you give one or more trusted people authority to make decisions on your behalf. In England and Wales the most common forms are Lasting Powers of Attorney. There are two main types:

Property and financial affairs - This allows your chosen attorneys to manage money, pay bills, deal with banks and investments and, where necessary, sell property on your behalf.

Health and welfare - This allows attorneys to make decisions about medical treatment, care arrangements and daily routines if you lack mental capacity in future.

You choose who to appoint as attorneys and can name replacements in case someone is unable to act later.

Key Features

You must have mental capacity when you create and sign the document.

Forms must be signed by you, your attorneys, witnesses and a certificate provider who confirms that you understand what you are doing and are acting freely.

The documents need to be registered before use.

Attorneys must always act in your best interests and, where possible, involve you in decisions.

Benefits of having Powers of Attorney in place

For you:

Peace of mind that someone you trust can step in if you become unable to manage your own affairs.

Confidence that your values around medical treatment, independence and dignity will be respected.

For your family:

Clarity about who is responsible for making decisions, which can reduce conflict.

The ability to access funds and deal with banks or utility companies without the considerable delay and cost of applying to the Court of Protection for authority.

For your wider plan, a financial advisor can:

Make Powers of Attorney a normal, caring part of financial planning, rather than something to be feared.

Help you think about who to appoint, and whether to separate roles between money and health decisions.

Coordinate with your solicitor to ensure that your Powers of Attorney, will and wider estate plan are all consistent.

Bringing it all together with professional advice

On your website you may want to close with a section that gently invites readers to take the next step. You might say something along these lines. When you look beneath the technical terms, inheritance tax and estate planning are really about love, responsibility and choice.

A financial advisor will:

Help you see clearly what you have and what you may need in your own lifetime.

Explain how the tax and legal systems work in plain language.

Work with your solicitor and, where needed, your accountant to design a joined up plan for wills, trusts, gifting and Powers of Attorney.

Review that plan with you as life unfolds, so that it stays aligned with your values.

Important note - This page gives general information about inheritance tax and estate planning in England and Wales based on the law and practice available at the time of writing. It is not personal tax, legal or financial advice. Tax and legal rules change and how they apply depends on your individual circumstances. Before taking any action, please speak to a regulated financial adviser and a qualified solicitor.